Update (28 July 2026): The government has removed the 15-month wait-out period for private property owners buying an HDB resale flat.

- If you’re a current or former private property owner of any age, you can now buy a non-subsidised resale HDB flat of any size with no wait-out period — as long as you don’t take an HDB housing loan (i.e. you pay with cash and/or a bank loan).

- A 30-month wait-out still applies if you buy with an HDB housing loan, or if you buy a subsidised flat (a BTO flat, or a resale flat bought with CPF housing grants).

- You still need to sell and dispose of your private property within 6 months of buying the HDB flat.

For the full breakdown of who this helps and what still applies, read our guide: 15-Month HDB Wait-Out Period Removed: Should You Sell Your Private Property Now?

So you’ve started thinking about maybe selling your condo and buying an HDB, but there are so many questions on your mind – “Am I eligible to own an HDB?”, “Do I need to pay extra fees?”, “How much time does all this take?”, “What should I do first?!”. The number of things to consider is honestly overwhelming for downgraders. To make your life a little easier, we’ve broken down and answered all the questions you might have in this Ultimate Guide.

In this article, we’ll discuss:

- Checking Your Eligibility

- Planning Your Financials

- What happens to my existing condo loan?

- What happens to my CPF?

- Do I need to pay Seller’s Stamp Duty (SSD) after selling my condo?

- How much loan can I get for my HDB purchase?

- Can I get a grant for buying an HDB?

- Do I need to pay Buyer’s Stamp Duty (BSD) when I buy my HDB?

- Do I need to pay Additional Buyer’s Stamp Duty (ABSD)?

- Do I need to pay Resale Levy?

- Making Decisions

- Taking Action

Singapore’s regulations for selling and buying are some of the most confusing, and you’re taking the right step to research first. If you need further help and advice, find Singapore’s best property agents experienced in downgrading, on Propseller. An accomplished agent will be key for you to get through this with minimal stress and maximum results.

1. Checking Eligibility

When downgrading from a condo to an HDB, the first thing to check is if you’re even eligible to own an HDB and if you are, when you can buy it.

a. Can I buy an HDB after selling my condo?

You can buy an HDB after selling your condo if you meet any of HDB’s eligibility schemes. Use the Housing Development Board’s HDB Eligibility Check tool as there are a number of eligibility schemes, as well as personal details (such as marital status, employment status and citizenship) and monthly income to verify against.

In addition, you need to not currently own another private residential property. If you buy your HDB flat before selling your condo, you must dispose of the private property within 6 months of the purchase.

Since 28 July 2026, there is no wait-out period for buying a non-subsidised resale flat without an HDB housing loan, at any age. A 30-month wait-out still applies if you take an HDB housing loan, or if you buy a subsidised flat (a BTO flat, or a resale flat bought with CPF housing grants).

HDB will also check if you are an essential occupier of an existing HDB flat, a DBSS flat or a resale flat. If so, further details such as whether the other property’s Minimum Occupancy Period (MOP) has been met, will be verified.

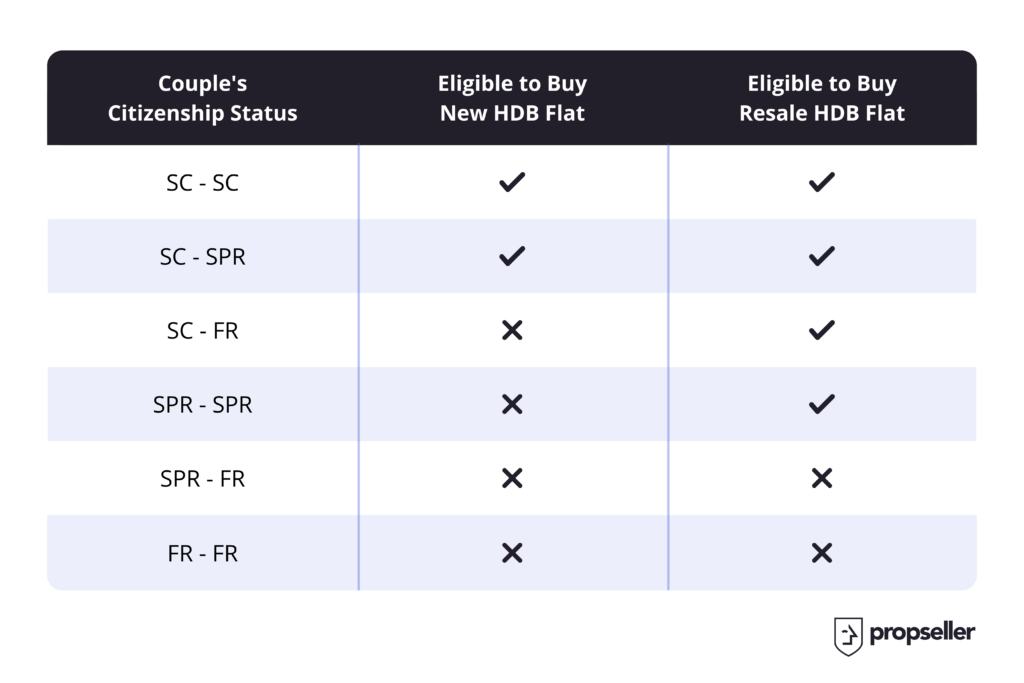

Based on the information provided, you will get a detailed recommendation generated by the system. Your marital status and your citizenship are the main factors considered.

If you’re single, you need to be at least 35 years old and a Singapore Citizen (SC) to buy a 2 room BTO flat or a bigger resale flat.

If you’re married, at least one of the two of you between you and your spouse needs to be an SC or both of you need to be Singapore Permanent Residents (SPR). If one of you is a foreigner (FR), the other must be an SC. See the table below for an overview of your eligibility to buy a new HDB flat vs a resale HDB flat.

There are several other eligibility criteria such as income ceiling, ethnicity, ownership status of other private or foreign properties and so on when it comes to buying an HDB, which you can read about on HDB’s site. If you need someone to analyse your specific case, you can ask us for free (or you can use the chat icon on the bottom right of your screen).

b. When can I buy an HDB after selling my condo?

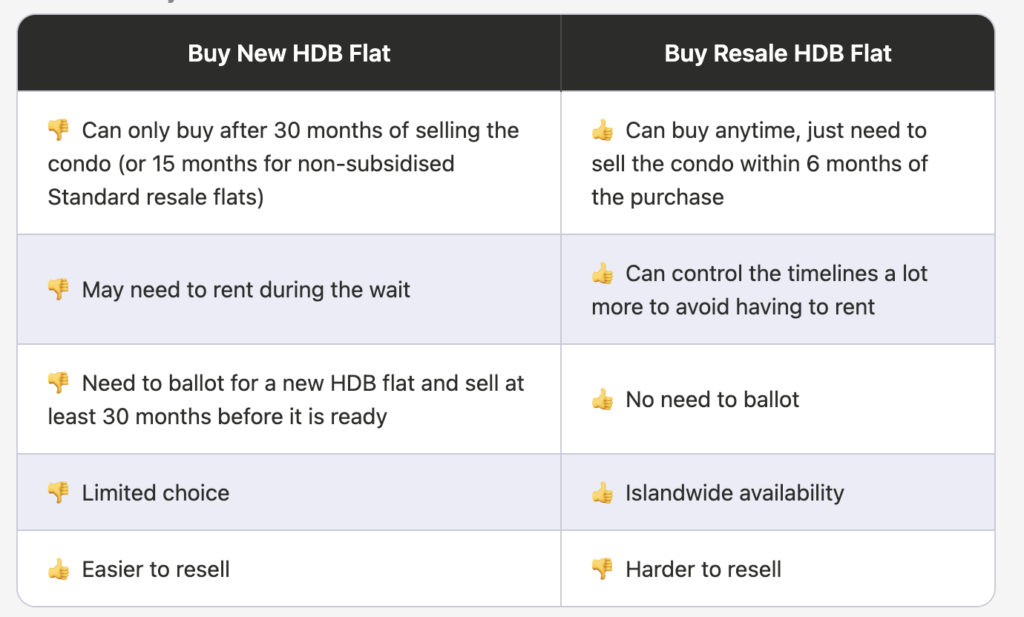

If you’re eligible to buy both a new HDB flat and a resale flat, which one should you go for and when can you buy it?

Most people in your position would buy a resale flat because of the differences listed below:

At this point, you need to decide if you want to wait a few years and get a new BTO flat or if you want something sooner and get a resale flat.

2. Planning the Financials

The second most important thing you need to do before making any decisions about downgrading from a condo to an HDB is to plan your finances.

a. What happens to my existing condo loan?

When you sell your condo, you have to pay off the loan that you took to purchase it. There are two things you need to take into account when it comes to your loan: the notice period and the lock-in period.

Notice Period

Typically, you need to give your bank 3 months notice that you will be paying your loan off early. If you provide less than 3 months notice, they may charge you a fee that is anywhere between $3,000 to a percentage (%) of your outstanding loan, for the shortfall in the notice period. However, this varies from bank to bank.

Lock-in Period

This is usually the first few years (1-5 years) of your loan during which the bank would give you specific interest rates (which could be flat, discounted or something else), but also would not allow you to pay it off early or switch banks. If you are still in your lock-in period for your loan, you may incur some prepayment penalties from your bank, which is typically 1.5% of the outstanding amount. If you are paying it off after your lock-in period, you do not have to pay any penalties. Note that the numbers and terms can vary bank to bank, so please check these in the Letter of Offer of your loan.

b. What happens to my CPF?

Every Singaporean wants to know what happens to their CPF, during each such transaction. Let’s demystify this below.

What happens to your CPF when you sell the condo

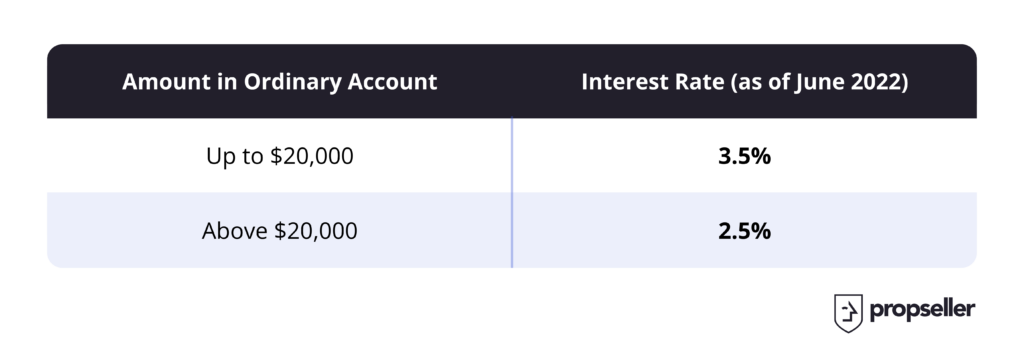

Many condo sellers overestimate the cash proceeds they will get from their condo sale. When your condo sale is executed, you have to “return” the CPF amount that you withdrew to make your condo purchase back to your CPF Account, with interest. However, it’s still your money and you can reuse it to purchase your HDB. The interest rates vary based on the amount in your account and your age.

You can log in to my CPF Online Services to view your accrued interest (under “My Statement”).

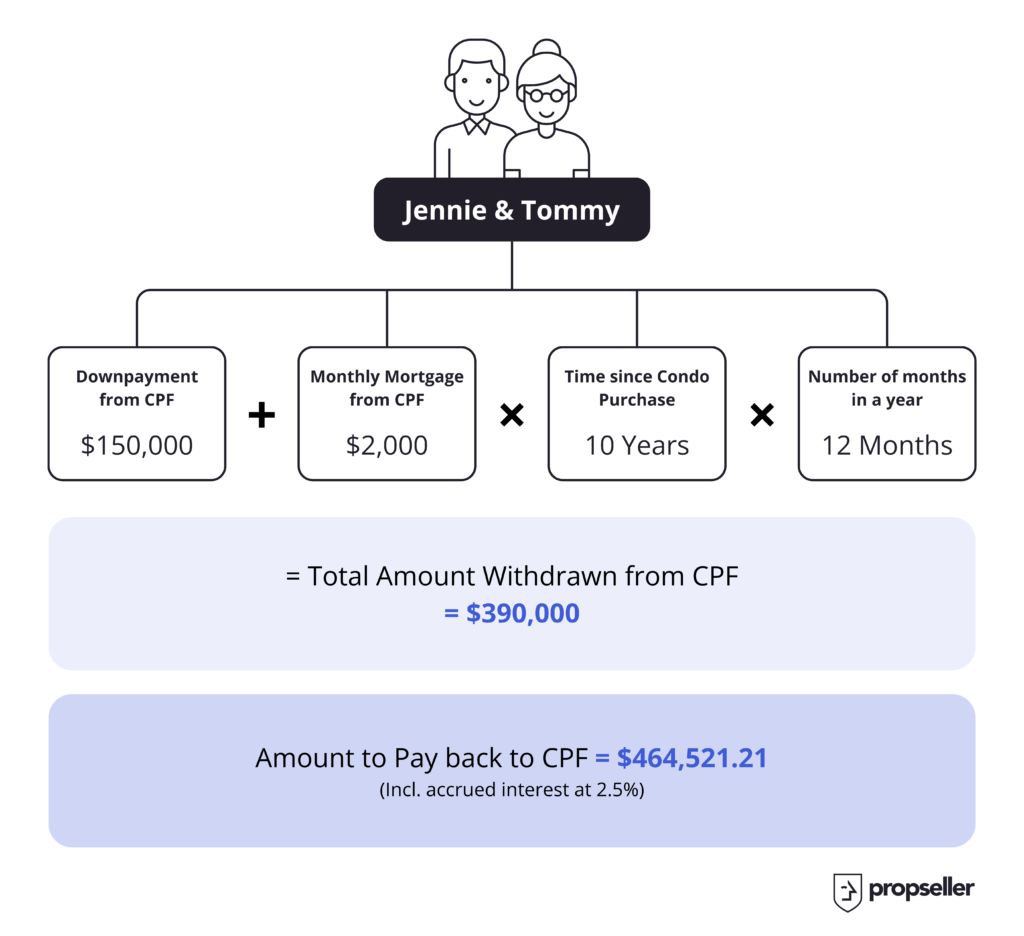

Case Study:

Let’s take the case of Jennie and Tommy, a married Singaporean couple, throughout this article. When Jennie (45 years old) and Tommy (50 years old) purchased their condo 10 years ago, they took money from CPF for the downpayment as well as for monthly mortgage payments. They had a minimum of $20,000 each still left in their accounts.

Hence, Jennie and Tommy will have to put almost $470,000 from the proceeds of their condo sale back into their CPF accounts, which they can use for purchasing their HDB or for retirement.

What happens to your CPF when you buy the HDB

On the 10th of May, 2019, the government passed new rules on how much CPF can be used for the purchase of your property.

The criteria are as shown below:

- The leasehold of the property must be such that the youngest owner of the property must be able to live up to the age of 95 years in it. If such a term can not be met, the amount of CPF available to be withdrawn will be pro-rated.

- You can withdraw up to 100% of the market value or the purchase price of the property from your CPF Ordinary Account (OA), whichever is lower.

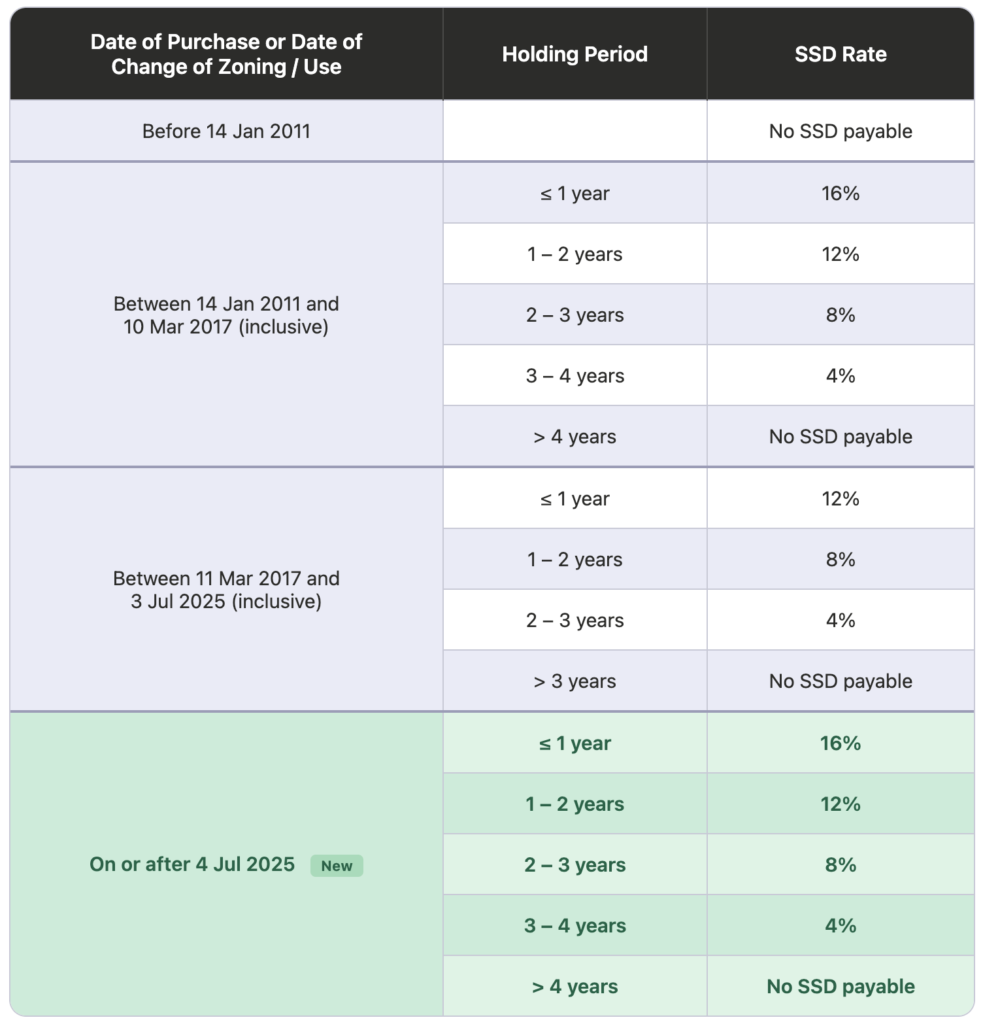

c. Do I need to pay Seller’s Stamp Duty (SSD) after selling my condo?

Whether or not you have to pay any Seller’s Stamp Duty (SSD) when selling your condo depends on when you bought it and how long you have held it. If you bought your property before 4 July 2025, the holding period is 3 years — sell after holding it for 3 years and you pay no SSD.

If you bought it on or after 4 July 2025, the holding period is 4 years, with SSD rates of 16%, 12%, 8% and 4% for a sale in the 1st, 2nd, 3rd and 4th year respectively (0% after 4 years). SSD is calculated on the actual price or the market value of the condo, whichever is higher

. Find out everything to know about Seller’s Stamp Duty (SSD) here.

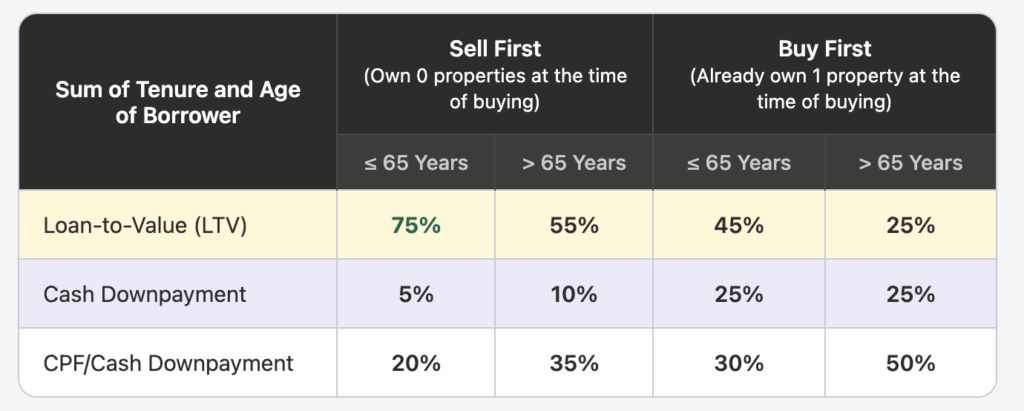

d. How much loan can I get for my HDB purchase?

If you sell your condo first before buying the HDB, you would have 0 properties in your name at the time of buying, so you can get a higher loan amount. If you buy first, you would already have 1 property (i.e. your condo that you haven’t sold yet), so the HDB would be your 2nd property at the time of buying. Banks will give you a higher loan amount if you own 0 properties compared to if you already own 1 property.

The bank loan rates you can get are as shown below:

Bank loan LTV limits were updated on July 6, 2018. The above table assumes you do not own any additional properties. If you own more properties, check the rates here.

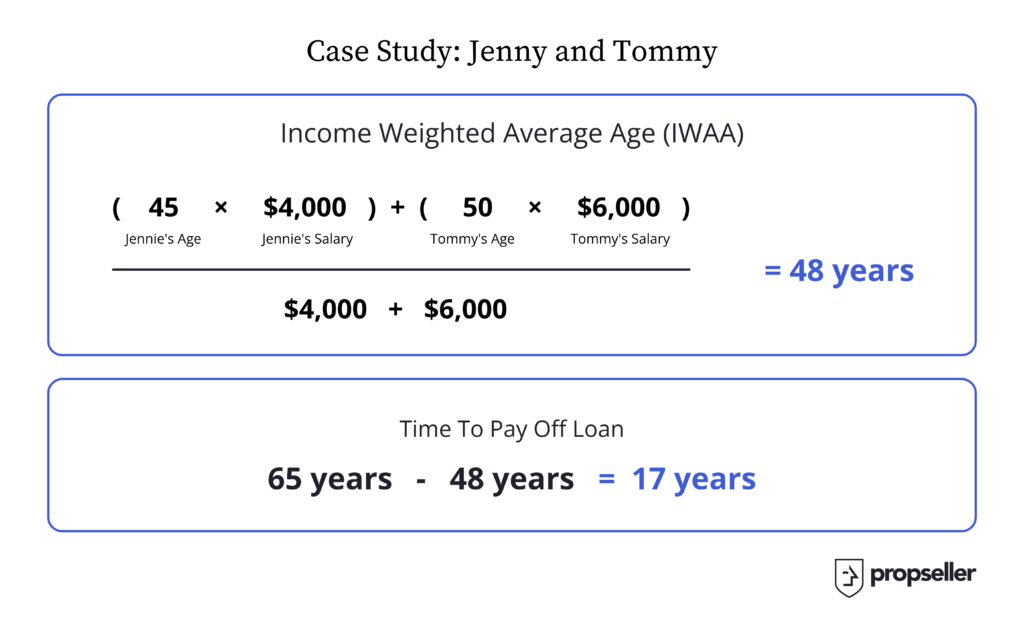

How does my age impact my loan?

Sellers can sometimes forget that their age matters a lot for their next purchase. The monthly mortgage for the property they want to buy next will be calculated based on it. You will be surprised at how high your mortgage can get when you’re older.

Since the “borrower” in your case is actually a couple, i.e. you and your spouse, your combined age is taken based on your income. It is called your Income Weighted Average Age (IWAA).

Case Study:

Jennie and Tommy’s “couple age” or their Income Weighted Average Age (IWAA) is based on their combined income and age as shown below:

If Jennie and Tommy take a 75% loan for their $500,000 HDB, this would mean:

Loan amount = $375,000

Assume interest rate = 2.0%

Since they only have 17 years to pay it off,

Their Monthly Mortgage Payment = $2,170

If they were younger and say they had 30 years to pay it off,

Their Monthly Mortgage Payment = $1,386

This is a difference of nearly $800 per month, which could have a huge impact on their cash flow. This calculation is hence crucial to complete, before making decisions on what you can afford to buy.

e. Can I get a grant for buying an HDB?

HDB offers many grants for making a purchase – for singles, orphans, first-time HDB applicants, families who want to live close to their parents or children and many others. They all have specific eligibility criteria which you can check on HDB’s site: for a resale HDB flat, for a new HDB flat.

Note that you can get a maximum of 2 such grants in a lifetime. As of August 2024, the maximum Enhanced Housing Grant (EHG) has been increased to $120,000 for families and $60,000 for singles.

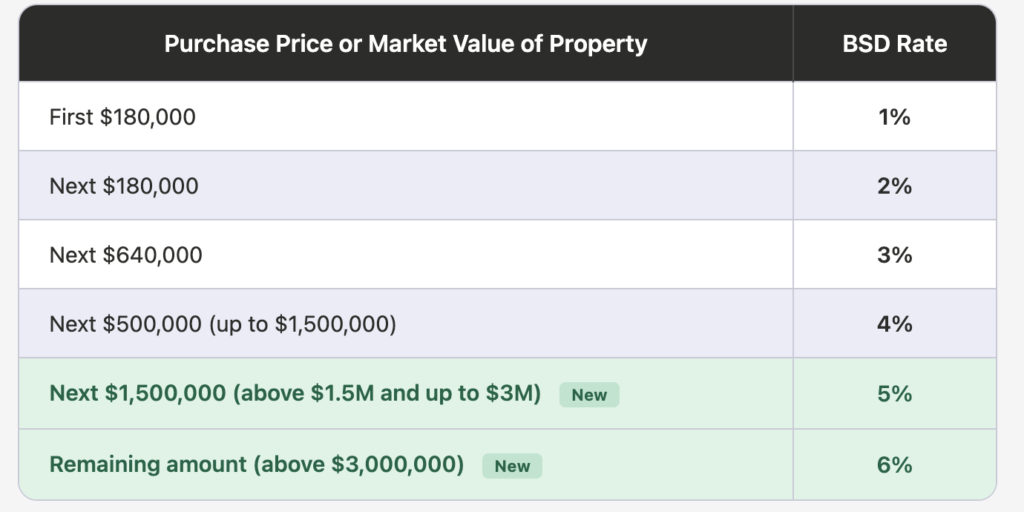

f. Do I need to pay Buyer’s Stamp Duty (BSD) when I buy my HDB?

Yes, you will have to pay a Buyer’s Stamp Duty (BSD) when you buy your HDB, which will be based on the purchase price or market value of the HDB you end up buying (whichever is higher). Find out everything you need to know about Buyer’s Stamp Duty (BSD) here.

The rates above were updated on 15 February 2023. The top marginal BSD rate for residential properties is now 6% (for the portion above $3 million) and 5% (for the portion between $1.5 million and $3 million). For HDB-priced properties under $1.5 million, the existing tiered rates of 1%–4% still apply.

g. Do I need to pay Additional Buyer’s Stamp Duty (ABSD)?

Additional Buyer’s Stamp Duty (ABSD) is charged on top of the standard Buyer’s Stamp Duty, and how much you pay depends on your profile and how many residential properties you’ll own.

The current ABSD rates took effect on 27 April 2023 and still apply. Singapore Citizens buying their first residential property pay 0%, and Permanent Residents buying their first pay 5%.

If you buy your HDB before selling your condo, you’ll briefly own two properties, so ABSD applies at the second-property rate – 20% for Singapore Citizens and 30% for PRs.

Married couples with at least one Singapore Citizen spouse can claim a refund of that ABSD if they sell their first property within 6 months of buying the second. Because rates change and depend on your citizenship and property count, check the current ABSD rates on the IRAS website, or ask us to work through your specific case.

Read more on IRAS website.

h. Do I need to pay Resale Levy?

The resale levy is meant to reduce the housing subsidy on the flat buyers’ second subsidised flat. It also ensures a fairer allocation of housing subsidies among flat buyers.

If you have already bought a subsidised housing, you will need to pay a resale levy when you buy a second subsidised flat. A subsidised housing is:

- A flat bought from HDB

- A resale flat bought with CPF housing grant

- A Design Build and Sell Scheme (DBSS) flat bought from a property developer

- An Executive Condominium (EC) unit bought from a property developer

- Other forms of housing subsidy (e.g. enjoyed benefits under the Selective En bloc Redevelopment Scheme (SERS), privatisation of HUDC estate etc.)

If you do not intend to buy a second subsidised flat from HDB, i.e., you are buying a resale flat or private residential property, you will not pay the resale levy.

The resale levy is a major factor to consider when buying your next HDB flat. To find out everything you need to know about it, have a look at our ultimate guide to the HDB and EC Resale Levy.

3. Making Decisions

Now that you have all these numbers ahead of you, what do you do with it?

Your next step is to check what you can afford and make decisions on what you need. The amount of cash and CPF you have available will be the determining factors on whether you are able to buy first or not.

a. Which HDB can I afford?

You first have to calculate the amount of money you have for the purchase, and also determine if you need extra cash for renovation, other investments, paying off debts etc.

Potential Cash Proceeds =

Condo Sale Price

– Outstanding Loan Amount

– CPF Refund

– Other Fees (Legal, Property Agent, Taxes, etc.)

Amount Available for Purchase =

Total CPF Balance Amount

+ Cash Proceeds

+ Loan

+ HDB Grant

– Buyer’s Stamp Duty (BSD)

– Additional Buyer’s Stamp Duty (ABSD)

– Other financial commitments

Case Study:

Jennie and Tommy have made the below decisions:

- Since they are already in or close to their 50s, they do not want to take any additional loans and add to their debts

- They want to save some cash for paying off outstanding credit card debts

- They want to sponsor their son’s university tuition fee

- They want to use their CPF for the purchase

Below are the typical HDB prices:

- Avg. Price of 3 Room HDB = $490,000

- Avg. Price of 4 Room HDB = $620,000

- Avg. Price of 5 Room HDB = $820,000

- Avg. Price of Executive Flat = $900,000

Note: These are approximate average prices as of 2025 and vary significantly based on location, flat age, floor level, and condition. Prices have risen substantially since 2022.

Based on their budget of $500,000, they can get a 4 or 5 Room HDB in 2022. In 2026, they could only get a 3 room flat.

b. Should I downgrade by selling my condo first or buy an HDB first?

The amount of money you have at hand plays a huge part in whether you sell first or buy first, but there are a few other pros and cons as listed below. They should help you decide on which one you should do first:

4. Taking Action

Depending on whether your eventual decision is to buy the HDB first or sell the condo first, the timeline of events may vary. However, the steps are the same and the most important ones are listed below.

a. Hire a property agent experienced in downgrading from a condo to an HDB

Your property agent’s skill is crucial to the success of your property sale and purchase. Given the number of frequently changing regulations there are to stay on top of, and the tight timelines you have to work with while downgrading from a condo to an HDB, you want someone who knows what they’re doing. Note that if you don’t already have one, you can find an experienced agent on Propseller.

Your agent will help you with:

- Checking your eligibility

- Completing your financial planning

- Determining which HDB to buy

- Deciding whether to sell your condo first or buy an HDB first

And everything that comes after.

b. Start marketing your condo for sale

A condo sale from start to completion can take anywhere between 3-6 months. Of course, there are the exceptional cases when it can be much earlier or much later based on the individual unit’s condition, the price set, the demand and supply in your area etc. The steps that take the most time are:

- Finding buyers (4-12 weeks)

- Handing over and transferring ownership (8-12 weeks )

See the timeline infographic below to see the individual steps to be taken during the sale and how long each step takes.

c. Start viewing HDBs to buy

A resale HDB purchase from start to completion can take anywhere between 2-3 months. The steps that take the most time are:

- Viewing, shortlisting and confirming the unit you want to buy (4 weeks)

- Handing over and transferring ownership (8-12 weeks)

- Optional: Renovation (8 weeks)

Note: If you need cash earlier because your purchase went through faster than your sale, you can get a bridging loan.

See the timeline infographic below to see the individual steps to be taken during the purchase and how long each step takes.

Note that these timelines are based on current market practice and regulations, and are subject to change case by case.

Conclusion

In conclusion, before you make any decisions on which home to buy, first check your eligibility, then calculate your finances, then check what you can afford and finally create an action plan. Downgrading from a condo to an HDB is a complex process with many regulations, but it can be simplified if you follow the steps above and have great professional help from agents and lawyers.

Have any questions about downgrading your condo? Ask us in the comments or on the chat icon on the bottom right of your screen!

Don’t have an agent yet? Find agents experienced in downgrading from a condo to an HDB on Propseller, to start your journey.

Disclaimer: All information and materials contained in these pages including the terms, conditions and descriptions are subject to change. In addition, we do not make any representations or warranties that the information we provide is reliable, accurate or complete or that your access to that information will be uninterrupted, timely or secure.

Whilst every effort has been made to ensure the accuracy of information on the Site, we do not warrant the accuracy, adequacy or completeness and expressly disclaim liability for completeness, accuracy, timeliness, reliability, suitability or availability with respect to the Site or the information and materials contained on the Site for any purpose.