You’ve decided that you want to buy a resale flat. Your first instinct is likely to search up PropertyGuru and to find your dream home – but hold your horses. Before you start your search and enquiring on shortlisted listings, there are a couple of other steps you need to take first!

P.S. if you’re looking to sell a HDB before buying one, you might want to read our full guide to selling a HDB first instead as you would almost always want to sell first before buying.

Buying a resale flat in 2026 involves 8 clear stages, from getting your eligibility letter to collecting your keys. From start to finish, most buyers should plan for 3 to 6 months: roughly a month for your HDB Flat Eligibility (HFE) letter, however long it takes you to find the right flat, and then about 8 to 12 weeks once you’ve secured an Option to Purchase. Here’s the full timeline at a glance:

| Stage | What happens | Typical time |

|---|---|---|

| 1. Get your HFE letter | Confirm your eligibility, loan amount, and grants | ~1 month |

| 2. Sort out financing & budget | HDB or bank loan, CPF, stamp duty, cash on hand | Alongside Stage 1 |

| 3. Search & view flats | Find a flat on the HDB Flat Portal | 2 weeks to a few months |

| 4. Get the Option to Purchase (OTP) | Seller grants you the OTP; you pay the Option Fee | 1 day |

| 5. Request for Value & exercise the OTP | Get HDB’s valuation, then commit | Within the 21-day option period |

| 6. Submit the resale application | Both you and the seller apply on the portal | Within 7 days of each other |

| 7. HDB approval & document endorsement | HDB accepts, you endorse documents and pay fees | ~8 weeks |

| 8. Completion & key collection | Final appointment, balance paid, keys handed over | On completion day |

That’s the bird’s-eye view. Now let’s walk through each stage so you know exactly what happens and the action(s) required on your end.

1. Get your HFE letter

Before you do anything else, apply for your HDB Flat Eligibility (HFE) letter through the HDB Flat Portal. The HFE letter is the single document that tells you three things you need before you start shopping: whether you’re eligible to buy a resale flat, how big an HDB housing loan you qualify for, and how much in CPF housing grants you can receive.

If you bought before 2023 and remember the old HLE letter (HDB Loan Eligibility), the HFE letter has replaced it. It’s a more complete, one-stop assessment of both your eligibility and your financing.

Two things worth knowing upfront:

- It takes about a month. HDB processes your HFE letter in around 21 working days once it has all your documents, so apply early.

- It’s valid for 9 months. That’s your window to find a flat and get to the application stage. (The validity was extended from 6 to 9 months back in November 2023.)

2. Sort out your financing and budget

Your HFE letter tells you what you can borrow. This step is about deciding how you’ll actually pay.

There are five pieces to get straight: your loan, your CPF, your stamp duty, your cash, and (for some buyers) whether a resale levy applies.

a. HDB loan or bank loan?

You have two financing routes, and you can only pick one.

An HDB concessionary loan charges 2.6% per annum (for January to March 2026) and lets you borrow up to 75% of the price or valuation, whichever is lower. The rate is pegged at 0.1% above the CPF Ordinary Account rate and has barely moved in over a decade, so it’s predictable.

A bank loan also caps out at 75% loan-to-value, but the rate floats with the market. In 2026, bank rates for HDB flats have dipped below 2%, which makes them cheaper than the HDB loan on paper right now. The trade-off: bank rates can rise, and once you switch from an HDB loan to a bank loan, you can’t switch back.

Either way, you’ll need to cover a 25% downpayment, which can come from your CPF or be paid in cash.

b. How much CPF can you use?

You can use your CPF Ordinary Account (OA) savings for the downpayment, the monthly instalments, and most of the upfront costs. For most resale buyers, CPF covers a big chunk of the purchase – but not every dollar (more will be covered in the grants and CPF section below).

c. Buyer’s Stamp Duty (BSD)

Everyone pays Buyer’s Stamp Duty when they buy property in Singapore, HDB flats included. BSD is tiered: you pay 1% on the first $180,000, 2% on the next $180,000, and 3% on the next $640,000 of the price or valuation, whichever is higher. These rates have been unchanged since 15 February 2023. Here’s how the common tiers stack up:

| Portion of price/valuation | BSD rate |

|---|---|

| First $180,000 | 1% |

| Next $180,000 (up to $360,000) | 2% |

| Next $640,000 (up to $1,000,000) | 3% |

| Next $500,000 (up to $1,500,000) | 4% |

| Next $1,500,000 (up to $3,000,000) | 5% |

| Remaining amount | 6% |

For example, on a $600,000 flat, your BSD works out to $12,600. Here’s the exact math:

| Portion of price | BSD Rate | Calculation | Payable BSD |

|---|---|---|---|

| First $180,000 | 1% | 1% * 180,000 | $1,800 |

| Next $180,000 | 2% | 2% * 180,000 | $3,600 |

| Next $240,000 | 3% | 3% * 240,000 | $7,200 |

| Total | $12,600 |

You pay it within 14 days of exercising the OTP, and you can use CPF for it.

d. A note on ABSD and the resale levy

Two extra costs that might apply, depending on your situation:

- Additional Buyer’s Stamp Duty (ABSD): A Singapore Citizen pays 0% ABSD on their first residential property, so most first-time HDB buyers pay nothing here. Permanent Residents pay 5% on their first property, and anyone buying a second residential property pays more.

- Resale levy: Good news for most buyers – the resale levy generally does not apply when you buy a resale flat on the open market. It only kicks in when a second-timer who previously enjoyed a housing subsidy buys another subsidised flat (a new BTO or an EC from a developer). If you’re a second-timer and unsure, read our full resale levy guide.

e. Cash over valuation (COV)

This is the portion that most first-time buyers overlook. Cash over valuation (COV) is the gap between the price you agree to pay and HDB’s official valuation of the flat. If you agree to $620,000 and HDB values the flat at $600,000, that $20,000 difference is COV.

Most importantly**, COV must be paid entirely in cash.** You can’t use CPF or your loan to cover it, because both are capped at the valuation, not the price. In a tight 2026 market, COV is back and can run anywhere from a few thousand to tens of thousands of dollars – so be sure to set cash aside for it just in case.

3. Search and view flats on the HDB Flat Portal

With your HFE letter in hand, you can finally commence house-hunting. The HDB Flat Portal is the official one-stop platform for this: verified resale listings, filters to show only flats you’re eligible for, and a personalised payment plan generated from your HFE letter.

The most important filter to apply at this juncture is:

- Ethnic Integration Policy (EIP) and SPR quota: Every block has limits on the proportion of flats owned by each ethnic group, and a separate quota for Singapore Permanent Residents. A flat can be perfect and still be off-limits to you if its block has hit your group’s quota. The portal flags this, so filter for it early and save yourself the heartbreak.

It’s free to search, contact sellers, and book viewings on the portal. You can do all of this yourself, though many buyers still engage an agent to handle viewings, negotiation, and the paperwork.

This is where Propseller comes in. Our buyer’s agents handle the legwork most people don’t have time for: shortlisting flats that actually fit your eligibility and budget, arranging viewings, reading the valuation and COV situation honestly, and negotiating the price down rather than letting you overpay in a hot market. Read more about how Propseller helps buyers or consider scheduling a free, non-obligatory phone consultation with our friendly consultants below to find out more directly!

4. Get the Option to Purchase (OTP)

Found the flat? The next step is to secure it with an Option to Purchase (OTP) – a legal document the seller grants you that gives you, and only you, the right to buy the flat at the agreed price for a set period.

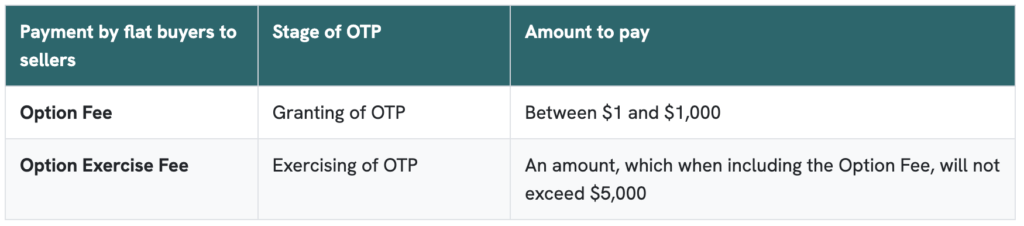

To get the OTP, you pay the seller an Option Fee. This is mutually agreed and can be anywhere from $1 to $1,000. Once you’ve paid and the seller signs, you have an exclusive option on the flat.

The OTP gives you a 21-calendar-day Option Period (this includes weekends and public holidays), and it expires at 4pm on the 21st day. During this window, the seller can’t sell to anyone else, and you decide whether to go ahead.

5. Request for Value and exercise the OTP

This is the stage buyers most often get wrong, so here’s the order that matters.

Once you hold the OTP, submit a Request for Value to HDB before you exercise the option. The Request for Value gives you HDB’s official valuation of the flat – and you need that number before committing, because it determines how much CPF and loan you can actually use (both are capped at the valuation) and therefore how much COV you’ll pay in cash. Submit the request by the next working day after the OTP date.

Once you have the valuation and you’re happy to proceed, you exercise the OTP: you sign it and pay the seller the Option Exercise Fee. This amount is mutually agreed, with one firm rule – the Option Fee and Option Exercise Fee combined cannot exceed $5,000.

Source: HDB

Exercising the OTP is the point of commitment. From here, you’re contractually bound to buy, and the stamp duty clock (14 days) starts ticking.

6. Submit the resale application

After you exercise the OTP, both you and the seller submit your respective halves of the resale application on the HDB Flat Portal. It’s a two-sided application: HDB only proceeds once both portions are in.

Two rules to remember:

- Submit within 7 days of each other. If one party submits and the other doesn’t follow within 7 calendar days, the application is cancelled with no refund. Coordinate with the seller (or your agents) so both sides go in close together.

- Pay the administrative fee. Each party pays a fee when submitting: $40 for 1- and 2-room flats, and $80 for 3-room flats and larger.

When you submit, you’ll also declare details like the manner of holding (if you’re buying with someone else) and any interest in private property.

7. HDB approval and endorsing your documents

Once both portions are in and complete, HDB reviews everything. HDB will notify you and the seller of its acceptance within 28 working days of receiving the complete application, by SMS and email.

From the date of acceptance, the processing phase runs for about 8 weeks. During this window:

- HDB prepares all the legal documents for the transaction.

- You’ll get an SMS telling you when to log in and endorse those documents – you have 6 days to do so once notified.

- You pay the conveyancing fees, stamp duties, and any other charges online.

- Both sides’ lawyers complete the title checks, and HDB sets a completion date.

8. Completion and key collection

The final stage. On the completion date, the transaction is finalised – typically at an appointment at the HDB Hub.

On the day itself:

- The balance of the purchase price is paid to the seller, drawn from your loan, CPF, and cash as planned.

- Ownership is legally transferred to you.

- The seller hands over possession and the keys.

That’s it – the flat is yours. From the day you exercised the OTP, this whole back half of the process typically takes 8 to 12 weeks, depending on valuation processing, loan approval, and the appointment slots available.

How much can grants and CPF actually cover?

If you’re a first-timer, this is where the buying process gets a lot more affordable. Eligible first-timer families can receive up to $230,000 in CPF housing grants when buying a resale flat, across three grants – the Family Grant, the Enhanced CPF Housing Grant (EHG), and the Proximity Housing Grant (PHG). The exact amount depends on your income, the flat size, and how close you live to family. Here’s how the three stack up:

| Grant | What it’s for | Amount |

|---|---|---|

| CPF Housing (Family) Grant | First-timer families buying resale | $80,000 (2- to 4-room) / $50,000 (5-room or larger) |

| Enhanced CPF Housing Grant (EHG) | Based on household income | Up to $120,000 (families) / up to $60,000 (singles) |

| Proximity Housing Grant (PHG) | Living near or with family | $30,000 (living with) / $20,000 (within 4km) |

A few things to keep in mind. The grants are paid into your CPF Ordinary Account, not as cash – they reduce how much you need to finance, but you can’t pocket them. Income ceilings apply to the Family Grant and EHG (the PHG has none). And the grants, like your loan and CPF, are tied to the valuation – so they don’t help with COV, which stays cash.

For the full eligibility breakdown and how the grants interact with your loan, see CPF’s official grant guide or HDB’s grant page.

FAQ

How long does it take to buy a resale HDB flat?

Plan for 3 to 6 months in total. Your HFE letter takes about a month, finding the right flat takes as long as it takes, and once you’ve exercised the OTP, the application and completion run roughly 8 to 12 weeks.

Can I buy a resale HDB without an agent?

Yes. The HDB Flat Portal lets you search, contact sellers, book viewings, and submit the resale application yourself, all for free. Many buyers still use an agent for the negotiation and paperwork, but it isn’t required.

What is COV and do I have to pay it in cash?

Yes, it must be paid in cash. Your CPF and loan are both capped at the valuation, so neither can cover the COV portion.

How much CPF can I use to buy a resale flat?

You can use your CPF Ordinary Account for the downpayment, stamp duty, and monthly instalments, up to the flat’s valuation. CPF can’t be used for COV, and there are withdrawal limits on older flats with shorter remaining leases.

What happens if my HDB loan is lower than the price?

Your loan is capped at 75% of the valuation, not the price. If the price is above the valuation, or your loan amount comes in lower than expected, you make up the difference with CPF and cash. This is exactly why you do the Request for Value before exercising the OTP, so there are no surprises.

How long is the HFE letter valid?

9 months from the date of issue. If it’s about to expire and you haven’t found a flat, you can apply for a fresh one.

Buying a resale flat isn’t that complicated once you can see the whole path – get your HFE letter, sort your financing, find your flat, secure it with an OTP, and let the application run to completion.

After all, the part that trips people up is rarely the steps. It’s the money portion, specifically with the financial planning. It’s the COV you didn’t budget for in cash, the loan that came in lower than hoped or the valuation you committed to without checking.

That’s where having someone experienced in your corner pays for itself. At Propseller, our agents help buyers find the right flat, read the valuation honestly, and negotiate a price that doesn’t leave you overpaying. Get a free consultation below to find out how we can assist you in your property journey!