The HDB resale market has been good to sellers for seven years. But the first cracks are showing — and the window to maximise your gains is narrowing.

Here are 5 reasons why you should sell your HDB right now.

1. HDB resale prices dipped for the first time in 7 years

For seven consecutive years, HDB resale flat owners have enjoyed one of the most remarkable property runs in Singapore’s history. Quarter after quarter, the HDB Resale Price Index (RPI) climbed — 20 consecutive quarters of uninterrupted growth.

If you owned an HDB resale flat during this period, you were getting wealthier every three months just because you owned a HDB flat.

That streak has now ended.

In Q1 2026, the HDB Resale Price Index recorded its first decline — a dip of 0.1%. A small number, yes. Easy to dismiss as noise.

But here’s the thing about momentum: it doesn’t announce itself when it breaks. That 0.1% dip isn’t just a statistic, it’s a signal.

The question isn’t how far prices have fallen. It’s whether you’re willing to bet they won’t fall further.

Markets don’t collapse overnight. What usually follows a long bull run is quieter and, honestly, more frustrating for sellers — a slow softening.

Prices drift sideways. Buyers start lowballing. Your flat sits on the market longer than expected.

You drop the price once, then again. Six months later, you’ve sold for less than a neighbour who moved a year earlier.

We don’t know for certain that prices will fall further. But we do know the momentum that carried the market for seven years has broken. And the sellers who come out ahead are rarely the ones who waited for absolute confirmation — they’re the ones who read the early signs and moved while buyers still believed in the upside.

Waiting for “more certainty” is a trap. By the time the trend is unmistakably downward — confirmed across two, three, four quarters — the buyers who were willing to pay peak prices will have already moved on.

The sellers who walk away with the highest gains are never the ones who waited for the absolute peak. They’re the ones who recognised that the first dip is rarely the last — and acted while buyers still believed in the upside.

2. MOP flat supply almost doubling this year

For the past few years, one of the forces driving HDB resale prices upward has been simple: there weren’t enough flats to go around. Sellers held the upper hand because supply was tight and demand was hungry.

That dynamic is about to change — dramatically.

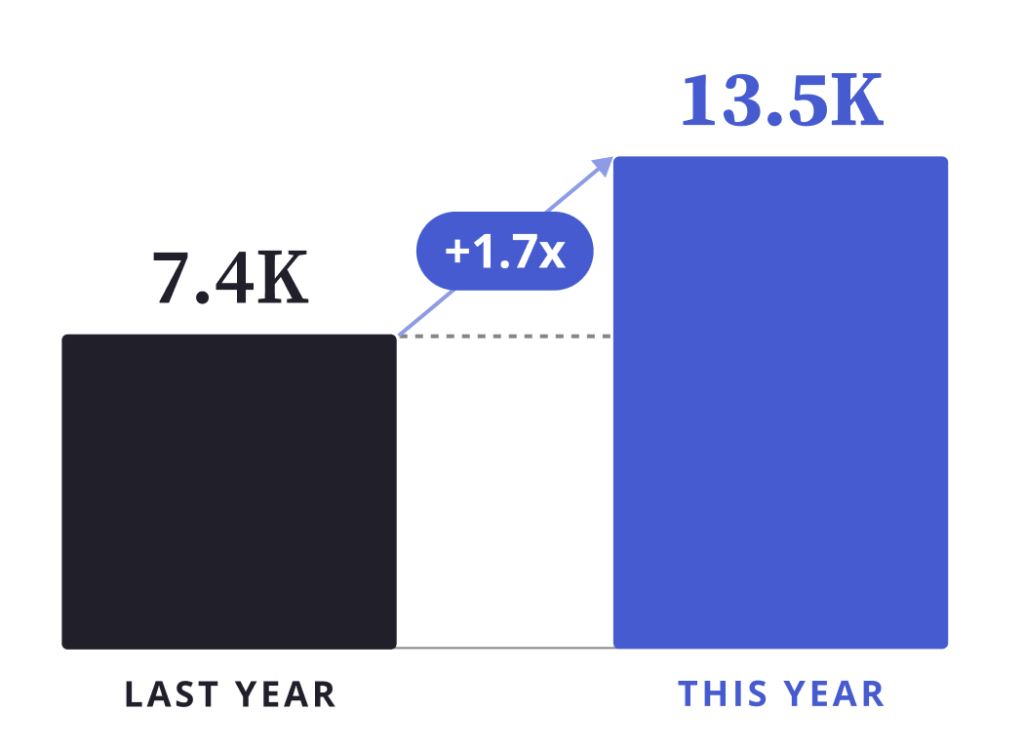

In 2026, approximately 13,480 HDB units will complete their Minimum Occupation Period (MOP) and become eligible for resale. To put that in perspective, that figure is roughly double the number of units that hit MOP in previous years.

In property, supply and demand is everything. And a doubling of HDB resale flats is a structural shift.

And it’s not happening in far-flung estates either. The bulk of these units are concentrated in areas buyers actually want — Queenstown, Bukit Merah, Kallang/Whampoa. Mature estates, central locations, addresses that have commanded strong premiums precisely because supply there has been tight.

Think about what happens when 50 of your neighbours all list their flats at the same time.

Suddenly, a buyer shopping in your estate has options. Genuine options. They can afford to walk away from your flat and view three others in the same afternoon. They can negotiate harder, offer lower, and wait you out — because they know another comparable unit will appear next week.

The bargaining power that sellers have enjoyed for seven years quietly passes to the other side of the table.

Right now, not all MOP-eligible owners have listed yet. That window — where you can get ahead of the wave rather than be swallowed by it — is still open. But it’s closing faster than most people realise.

Selling now means selling before your flat becomes one of dozens competing for the same pool of buyers. Waiting means becoming part of the surplus.

3. BTO waiting times have shortened to as low as 3 years

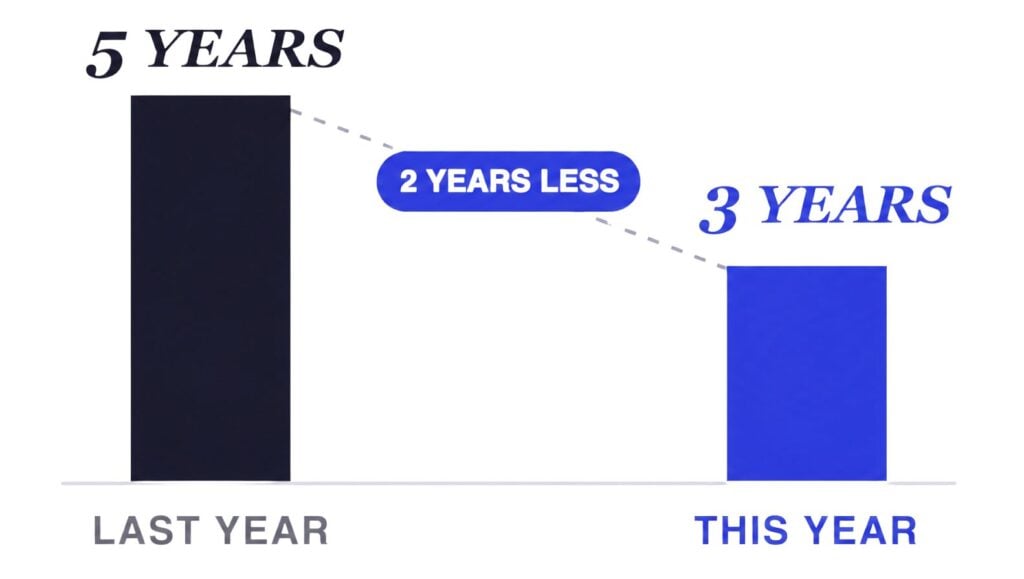

Cast your mind back to 2020, 2021, 2022. The resale market was on fire, and a big reason why was this: buyers were desperate. BTO wait times had ballooned to 5, sometimes 6 years.

For young couples who needed a home now — newlyweds, growing families, couples tired of living with parents — waiting half a decade for a BTO simply wasn’t an option. So they turned to the resale market, and they paid for the privilege.

That desperation was your resale premium. And it is quietly disappearing.

In June 2026, HDB is launching 6,900 new BTO units across Singapore. More importantly, many BTO projects today come with wait times of 3 to 4 years. Some are as short as 2. The government’s push to accelerate BTO supply — a direct policy response to the post-pandemic housing crunch — has fundamentally changed the calculation for first-time buyers.

Why pay a resale premium when a brand-new flat is only 3 years away?

This is the question every potential buyer of your flat is now asking themselves. And increasingly, the honest answer is: there isn’t a compelling reason to. A buyer who can wait 24 to 30 months gets a brand-new flat, full CPF housing grants, and a fresh 99-year lease — all at a significantly lower price than a resale unit in the same general area.

The “urgency” that once pushed buyers into the resale market, willing to stretch their budgets and overlook imperfections, has been replaced by patience and optionality due to even more supply in the market.

The pool of “urgent buyers” — the ones who drove COV figures to record highs — is shrinking with every BTO ballot.

What remains is a more measured, more selective buyer. One who compares carefully, negotiates confidently, and feels no particular pressure to commit quickly. These buyers are not bad buyers — but they are not the same buyers who fuelled the resale boom.

The window where resale flats commanded a genuine premium over BTO — because BTO was slow, uncertain, and scarce — is closing. With 6,900 units launching in June alone (after 9,000 units in Feb 2026), and many projects delivering in under 3 years, every month you wait is a month in which another wave of buyers quietly pivots away from resale and toward BTO.

This number hasn’t even included the October 2026 launch yet, with an estimated remainder of 4,000 BTO units available for sale in 2026.

4. Interest rates are at their lowest in years, and are expected to climb back up

Here is something most sellers never think about: your flat isn’t just worth what it’s worth. It’s worth what a buyer can afford to pay for it. And what a buyer can afford to pay is highly correlated with the interest rates.

Under HDB’s Mortgage Servicing Ratio (MSR) rules, buyers can only use up to 30% of their gross monthly income to service their housing loan. The interest rate directly determines how large a loan that 30% can support. When rates are low, each dollar of monthly repayment stretches further — meaning buyers qualify for larger loans, carry larger budgets, and can offer more for your flat.

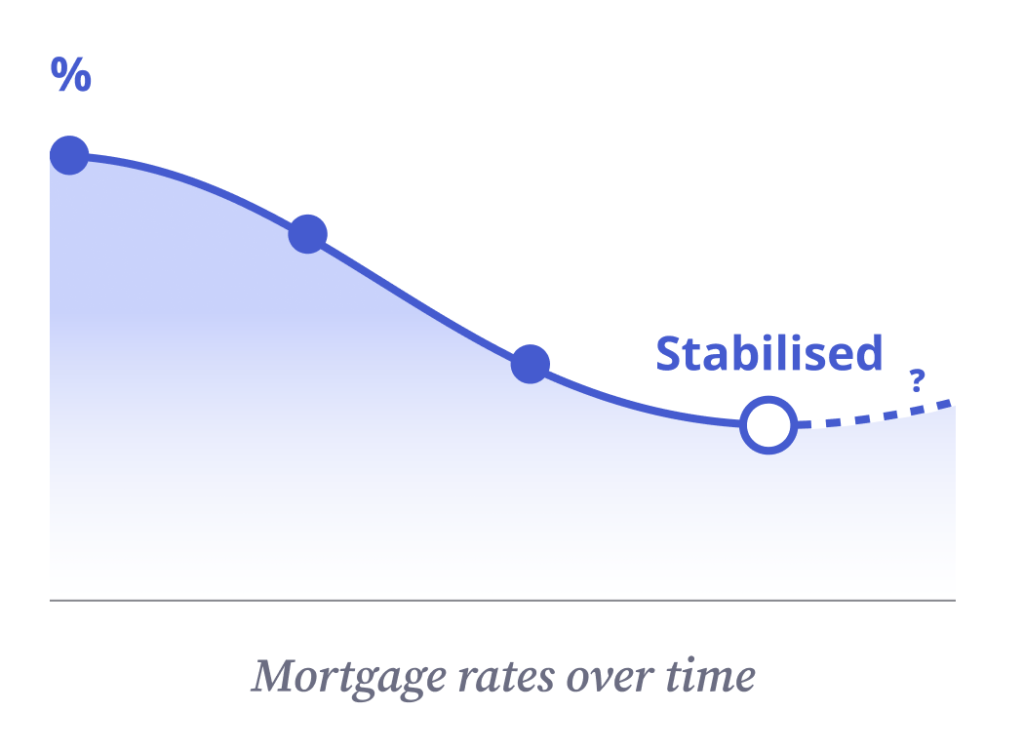

Right now, bank loan rates are sitting at 1.4% to 1.6% — a 3-year low. That is one of the most powerful situations a seller could ask for.

To make this concrete: a household earning $8,000 a month, borrowing at 1.5% interest over 25 years, can take a loan of approximately $570,000. That same household, borrowing at 2.5%, qualifies for roughly $510,000. That is a $60,000 difference in purchasing power — simply from a 1% shift in interest rates.

Your flat didn’t change. The buyer didn’t change. But what they can offer you changed by $60,000.

At today’s rates, buyers are walking into the market with the largest budgets they’ve had in two years. That translates directly into stronger offers, fewer negotiations that fall apart at valuation, and buyers who can stretch just a little more to close the deal at your asking price.

But this window is not guaranteed to stay open.

Interest rates are shaped by forces beyond any individual buyer or seller — global inflation pressures, US Federal Reserve policy decisions, and MAS’s own monetary stance. Singapore’s inflation, while easing, has not been fully tamed. If macro conditions shift — and in today’s extremely uncertain global climate, they can shift faster than anyone anticipates — rates can start climbing again.

Even a move from 1.5% to 2.5% quietly strips tens of thousands of dollars from your buyer’s budget without either of you fully noticing until the offer comes in lower than expected.

There is also a subtler risk. When borrowing costs rise, some buyers don’t just offer less — they exit the market entirely. They decide to wait, to save more, to ballot for a BTO instead.

And a smaller buyer pool, as any seller knows, means less competition for your flat and less urgency to offer well.

The sweet spot you are sitting in right now — low rates, high buyer budgets, strong purchasing power — is a gift. But gifts have expiry dates.

Selling today means selling to buyers who can afford to pay you well. Waiting means gambling that rates stay low, that buyer budgets hold, and that no policy shift between now and your eventual listing date quietly erodes the offers you would have received today.

The market is rarely this accommodating to sellers all at once. Take it while it lasts.

5. The cost of upgrading is as low as it’s likely to get

This is for the HDB owners who are looking to upgrade their homes. For some, selling their HDB was never about cashing out — it’s about moving up to a condo or even a landed property.

Here’s the part most people get wrong. They assume that because their HDB has appreciated, the upgrade has gotten easier.

Not necessarily. What decides whether you can afford the move isn’t your flat’s price tag — it’s the gap between what your HDB sells for and what your next home costs. That gap is the cash you actually have to bridge, and it’s the number that matters.

Right now, that gap is about as narrow as it’s likely to get. Your HDB is sitting at the top of a seven-year run, so the proceeds you can put toward your next home are near their peak. Sell today and you secure that gain at a known number — money that goes straight toward your downpayment, ABSD, and renovations.

Wait, and you give up that certainty. You’re betting on two separate markets — where HDB goes and where private goes — both moving in your favour at the same time. HDB has already shown its first crack in seven years. That’s not the moment to gamble that the maths will be friendlier later.

And here’s what makes the timing unusual: the buy side of your move is in your favour too. With private supply at multi-year highs and sellers actively negotiating, now is shaping up to be a buyer’s market for private property — so you’re not just selling your HDB near its peak, you’re stepping into your next home with real negotiating room.

So the real question isn’t whether your HDB is worth more than it was five years ago. It’s whether the full move — sell high, buy smart — is more achievable today than it’s likely to be once these windows close.

So, should you sell your HDB now?

Yes you should sell your HDB now. The signals are aligned in a way that rarely happens all at once. HDB price momentum has broken. Supply is about to flood the market. BTO wait times have collapsed, shrinking your buyer pool. And the interest rate tailwind that is putting strong offers on the table today is not guaranteed to last.

Waiting for more certainty is the one luxury the current market cannot afford you.

The sellers who maximise their gains are the ones who move while conditions still favour them — not after the shift becomes undeniable. That moment, for the HDB resale market, appears to be now.

If you are thinking about selling your HDB, the best next step is a conversation.

Talk to a Propseller agent today — get a free, no-obligation assessment of your flat’s value, your upgrade options, and the right timeline for your situation.