For seven years, the HDB resale market belonged to sellers.

Bidding wars, cash-over-valuation, and relentless price growth made buying feel like a losing battle.

That’s changed.

Here’s why the window that’s opened for buyers is one worth acting on.

1. The 7-year seller’s market is over

For seven years, buying an HDB resale flat felt like a negotiation you were destined to lose.

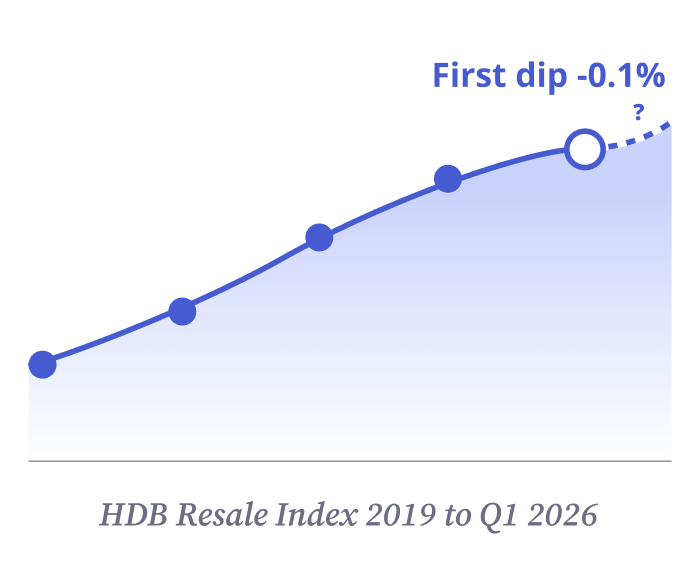

From 2020 to end-2025, the HDB Resale Price Index climbed roughly 55% — twenty consecutive quarters of uninterrupted growth. Every buyer who hesitated watched prices move further out of reach.

Cash-over-valuation became the norm, not the exception. Sellers received multiple offers within days of listing. Walking away from a unit meant watching it close at a higher price than you refused to pay, and starting the whole exhausting process again.

That era is over.

In Q1 2026, the HDB Resale Price Index posted −0.1% — the first quarterly decline since Q1 2019. A small number on paper. But what it represents is a shift that every buyer in the market right now should pay attention to.

For seven years, sellers held every card because buyers believed one thing above all else: prices will be higher next quarter. That belief drove FOMO, fuelled bidding wars, and pushed cash-over-valuation figures to record highs. The moment that belief breaks — and it has broken — the entire psychology of the transaction shifts.

Sellers know it too. The flat that would have had five offers in 2023 is sitting longer on the market today. Asking prices are being revised. COV demands that were non-negotiable twelve months ago are now opening positions in a conversation. For the first time in years, buyers are coming to the table with something they haven’t had in a long time — leverage.

This didn’t happen by accident. The government has been deliberate about cooling the market: increasing BTO supply, reviewing income ceilings, tightening loan-to-value ratios.

But that doesn’t mean that the HDB Resale Price Index will continue dipping.

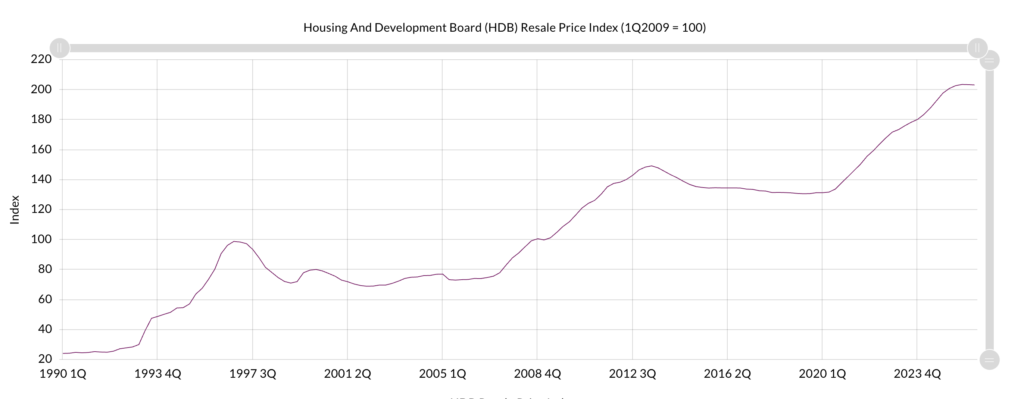

Looking at the long-term trend, dips in the Price Index did not guarantee that prices would go down. In fact, from the table above, you can see that prices continued climbing.

And with a 6.11mil population in Singapore, growing at 1.2% from June 2024 – June 2025, there is a large possibility that the demand for HDB resale will continue going up.

So if you want to take advantage of the dip, now is the time to do so.

2. The MOP supply surge

If the price index shift gives you confidence, what’s happening on the supply side should give you options.

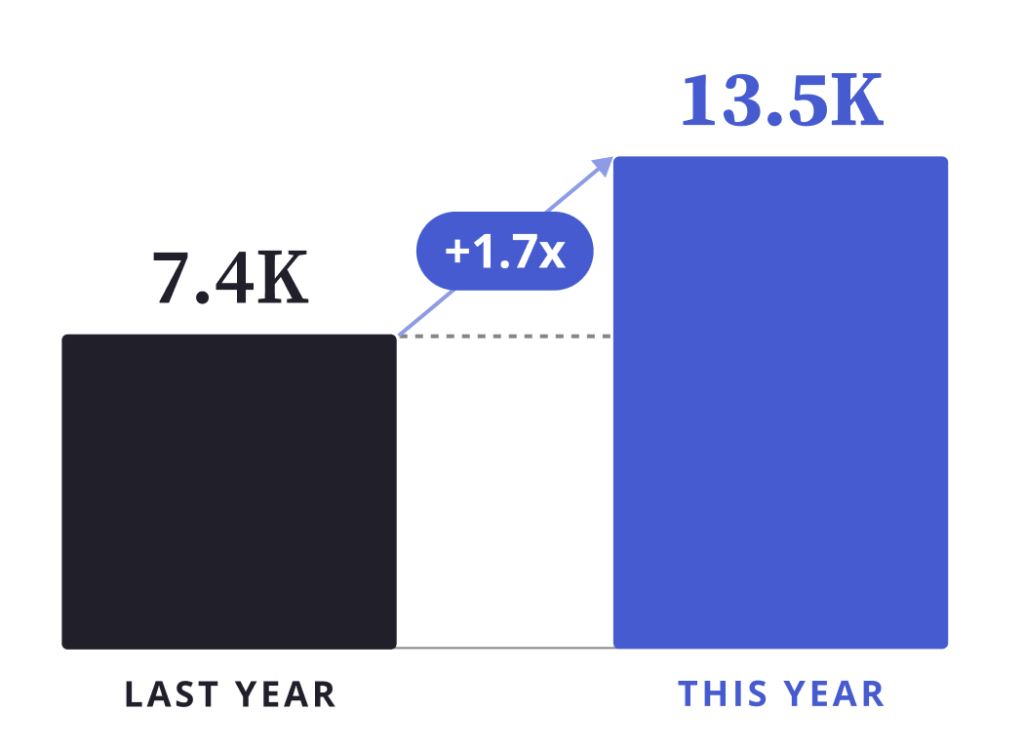

In 2026, approximately 13,500 HDB units are completing their Minimum Occupation Period and becoming eligible for sale on the resale market. Last year, around 7,400 units hit MOP. This year’s figure is nearly double — an 82% surge in a single year.

This isn’t a coincidence. These are the 2020 and 2021 BTO completions hitting their 5-year mark. During the pandemic, HDB launched unusually large BTO exercises to meet surging housing demand. That bulge in completions is now ripening into resale eligibility all at once — and it’s creating the most choice-rich resale environment buyers have seen in years.

What does that actually mean if you’re shopping for a flat right now?

It means you don’t have to settle. For the past several years, buyers in popular estates faced a simple reality: there weren’t enough units to go around, so you took what you could get, at the price being asked, before someone else did. That scarcity drove decisions that many buyers later regretted — overpaying for a unit they weren’t fully sold on, in a location that was their third choice, because waiting felt too risky.

That pressure is lifting. More listings mean genuine comparison shopping. You can view three units in the same estate on the same weekend, walk away from one that doesn’t feel right, and know another will appear next week. Sellers facing more competition with each other are listing days — and weeks — longer than before, giving you time to think rather than react.

One thing worth being clear about: more supply doesn’t mean prices are about to crash. It means the scarcity premium that sellers have enjoyed — the invisible surcharge you paid simply because there was nothing else available — is fading. Prices may stay relatively flat. But the value you get for your dollar improves meaningfully when you have real options and real negotiating room.

3. Interest rates have finally stabilised

Most buyers focus almost entirely on the purchase price when they’re working out affordability. The number that actually determines how much your home costs you over time — the interest rate on your loan — gets far less attention than it deserves.

Right now, that number is doing something very much in your favour.

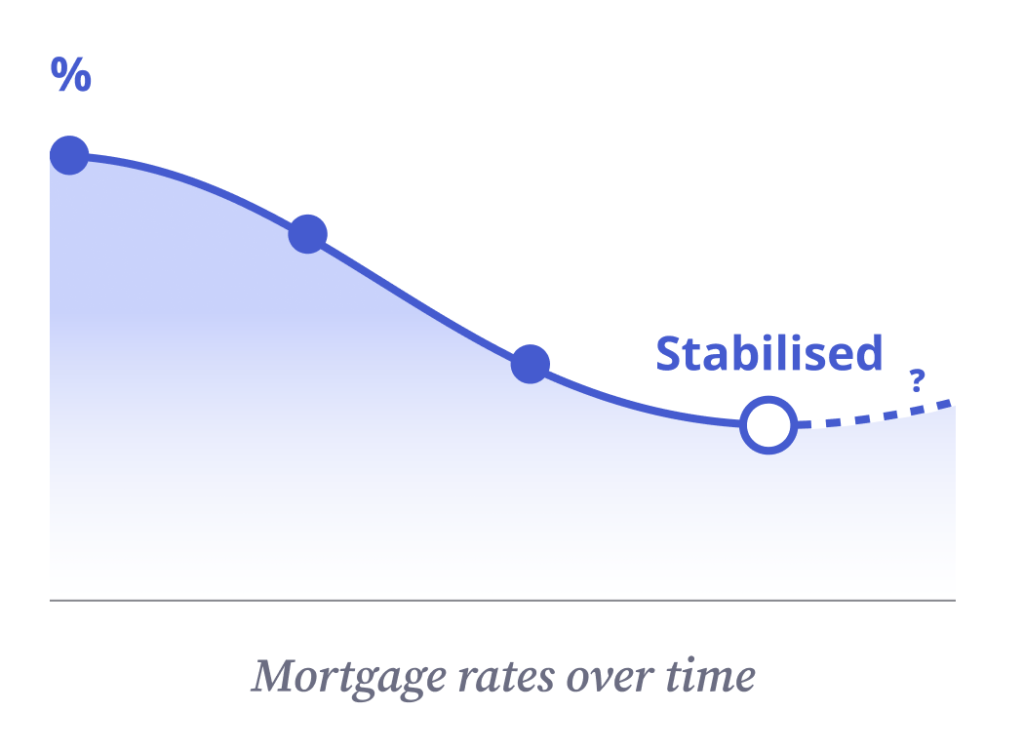

Bank fixed-rate mortgage packages are currently sitting at approximately 1.5% — a level that, after the aggressive rate hiking cycle of 2022 and 2023, most buyers weren’t sure they’d see again this soon. SORA has stabilised, banks are competing hard for mortgage business, and the result is some of the most attractive financing conditions the resale market has seen in years.

For comparison, the HDB Concessionary Loan rate — the government loan option that many buyers default to for its simplicity and security — sits at 2.6%. It’s pegged to the CPF Ordinary Account rate plus 0.1%, and it hasn’t moved meaningfully in years.

That 1.1 percentage point gap between the two options translates into real money. A lot of it.

Take a $600,000 resale flat financed over 25 years. At the HDB concessionary rate of 2.6%, your monthly instalment works out to approximately $2,720. At a bank rate of 1.5%, that same loan costs you roughly $2,400 a month. That’s a difference of $320 every month — or $3,840 a year — or just under $96,000 over the full loan tenure.

The same flat. The same purchase price. A $96,000 difference in what you actually pay, determined entirely by which loan you choose and when you choose it.

What matters most is this: the rate environment you are borrowing in today is genuinely favourable. The 2022-2023 hiking cycle pushed many buyers to the sidelines. Those who held off are now re-entering a market where financing costs have come down significantly — and that reduction in borrowing cost is, in many cases, worth more in real dollar terms than waiting for a further dip in purchase price.

Rates won’t stay here forever. The window where a bank loan saves you nearly $100,000 over the life of your mortgage is open right now.

Should I wait for prices to drop further?

It’s the question every buyer is asking right now. And it deserves an honest answer.

Probably not. And here’s why.

The Q1 2026 dip of 0.1% sounds meaningful when you read it as a headline. In dollar terms, on a $600,000 flat, it translates to $600. Most buyers spend more than that on legal fees alone. If you’re waiting for that 0.1% to become 2% or 3% before you commit, you’re betting on a further drop of $12,000 to $18,000 — while paying rent, losing the current financing advantage, and hoping nothing else in the market shifts against you in the meantime.

HDB resale prices have only seen sustained multi-quarter declines under extraordinary conditions — the 2013 to 2019 period, when the government layered cooling measure on top of cooling measure including significant ABSD increases.

Even then, the cumulative decline was modest, and buyers who timed it perfectly were the exception, not the rule. Most buyers who waited for the bottom ended up buying after the rebound had already started — paying more than they would have at the point they first hesitated.

Nobody calls the bottom in real time. It only looks obvious in hindsight.

But the more immediate cost of waiting isn’t about price at all. It’s about everything else that’s working in your favour right now that isn’t guaranteed to last.

If you’re currently renting while waiting for prices to fall, the math works against you faster than most people realise. At $2,500 a month in rent, you’d need HDB resale prices to drop by roughly $30,000 just to break even after a single year of waiting. That’s a 5% price decline on a $600,000 flat — historically unusual for the HDB resale market in anything other than a severe policy-driven correction.

Then factor in the rate risk. Bank loan rates are sitting at approximately 1.5% today. If macro conditions shift and rates climb back toward 2.5%, the increase in your monthly instalment on a $600,000 loan over 25 years wipes out far more in savings than any modest price decline would have delivered.

You’d have waited, paid rent, and still ended up paying more — just spread differently across time.

And the supply picture that’s currently so favourable to buyers is cyclical, not permanent. The 2026 MOP surge is a one-time bulge from the pandemic-era BTO completions. Once that wave is absorbed over the next 12 to 18 months, the pipeline narrows again.

The choice and negotiating room buyers have today won’t automatically be there in 2027.

So, should you buy an HDB resale flat now?

Yes — and the conditions haven’t been this favourable for buyers in seven years.

The seller’s market that defined resale HDB from 2019 to 2025 has hit its first real inflection point. Prices have plateaued. Supply is surging. Financing costs are at multi-year lows. The FOMO, the bidding wars, the cash-over-valuation demands — that era is behind us. What’s replaced it is a market where buyers can negotiate, compare, and make considered decisions without the constant pressure of being outbid.

That doesn’t mean prices are about to collapse. It means the balance of power has shifted — quietly but meaningfully — in your favour. And that shift won’t last indefinitely.

If buying an HDB resale flat has been on your mind, now is the time to move from thinking to doing.

Talk to a Propseller agent today — get a free, no-obligation assessment of your budget, your options, and the right estates to target based on where the MOP supply surge is greatest.