For years, buying private property in Singapore meant competing hard, moving fast, and paying whatever the market demanded.

That’s no longer the case.

Supply is at multi-year highs, sellers are negotiating, and financing conditions are the most favourable they’ve been since before the rate hiking cycle. Here’s what the data is telling buyers in 2026.

1. 58,000 more units for buyers

For most of the past decade, buying private property in Singapore felt like chasing a moving target. Supply was thin, developers held firm on prices, and the few resale units worth considering attracted multiple offers within days of listing.

Buyers who hesitated lost out. Buyers who stretched their budgets often had no choice.

That dynamic has shifted — and most buyers haven’t noticed yet.

Singapore’s private residential pipeline currently sits at approximately 58,000 units — roughly 50% above the 10-year average. These are units under active construction across roughly 20 projects scheduled to launch through end-2026, on top of thousands of resale units already on the market.

For the first time in this cycle, buyers have genuine choice — across geographies, price points, and developers who are actively competing for sales.

That last part matters more than most buyers realise. A significant portion of this pipeline comes from GLS sites that were tendered in 2021 and 2022, when land bid prices were aggressive. Developers paid premiums for that land and now need to move units.

That changes their posture. Developers who were content to hold firm on pricing in a thin-supply market are now offering early-bird discounts, absorbing stamp duties, throwing in furnishing packages — doing whatever it takes to keep sales momentum going. When developers compete, buyers benefit.

The resale market feels it too. When new launches flood the market with attractive options, resale sellers face a simple problem: their unit has to justify itself against something brand new. The result is a resale segment where motivated sellers are quietly accepting below-asking offers.

If you’ve been watching the market and wondering why some listings seem to linger, this is why.

The pipeline that’s creating all this choice is finite. Once these units are absorbed — typically within 18 to 24 months — supply tightens again and the leverage shifts back to sellers. This isn’t a permanent state. It’s a window.

And right now, that window is wide open.

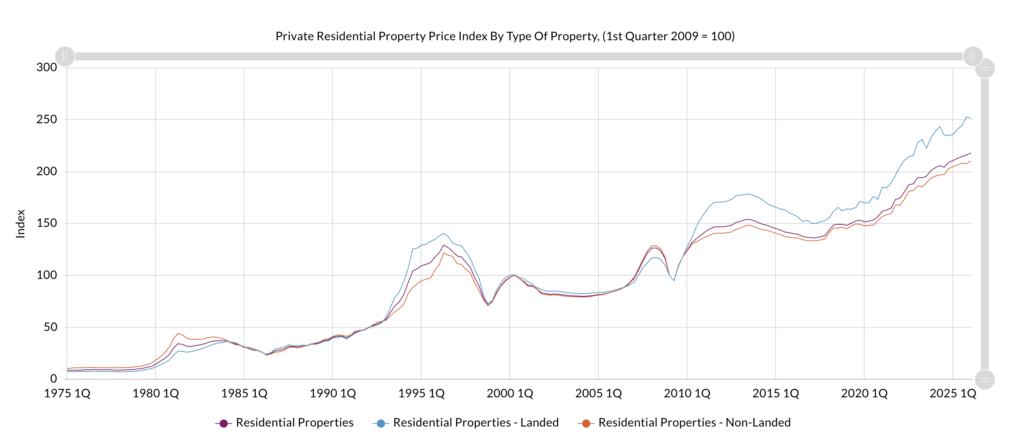

2. The Private Property Price Index increased, but transaction volumes have decreased

The URA Private Property Price Index rose 0.9% in Q1 2026 — roughly in line with the 0.8% average across 2025. If you’re a buyer who has been sitting on the sidelines waiting for prices to dip, that headline might feel discouraging.

It shouldn’t. Because the story behind that number is actually one of the strongest arguments for buying now.

Sitting behind that stable price index is a pipeline of approximately 58,000 units — 50% above the 10-year average — all under active construction with TOP dates approaching. These units haven’t hit the market yet. But they will. And when they do, they will do what supply always does when it arrives in volume — give buyers more options, more leverage, and more room to negotiate.

Price indices respond to supply with a lag. What reads as 0.9% growth today reflects transactions that closed months ago, before the full weight of this pipeline was visible. What the index will reflect 12 to 18 months from now — when tens of thousands of completed units are actively competing for buyers — is a different question entirely.

The smart buyer doesn’t wait for the index to confirm what the supply data is already telegraphing. By the time the price decline shows up in the official numbers, the best units will have already transacted — bought by buyers who read the pipeline early and moved while sellers were still anchored to yesterday’s prices.

Prices look stable today because the supply hasn’t landed yet.

Buy now, while sellers still believe the old market exists — and before the index catches up with what 58,000 units will do to it.

To pile on, the overall trend across all private property types seems to point in one direction – up.

Looking at the long-term trend, dips in the Private Residential Property Price Index did not guarantee that prices would go down for extended periods of time. In fact, from the table above, you can see that prices continued climbing. Don’t forget that the price index is a lagging indicator – so by the time you decide to wait, it might be too late.

And with a 6.11mil population in Singapore, growing at 1.2% from June 2024 – June 2025, there is a large possibility that the demand for private properties will continue going up.

So if you want to take advantage of the dip, now is the time to do so.

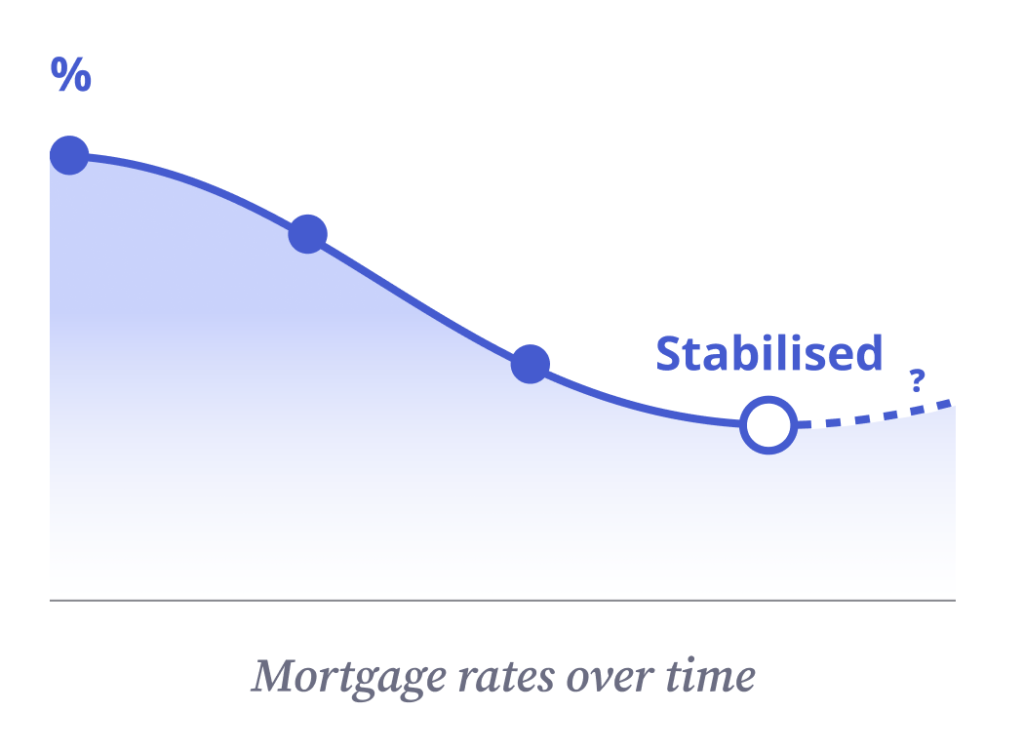

3. Singapore interest rates have stabilised, giving you more purchasing power

For private property buyers, interest rates are probably the single biggest variable in what your home actually costs you over time. And right now, that variable is sitting at levels that buyers who were active in 2023 and 2024 would have found hard to imagine.

Bank fixed-rate mortgage packages are currently available at approximately 1.5% to 2.0%. Floating SORA-based packages are in a similar range depending on bank spreads.

Compare that against the peak of the 2022 to 2024 hiking cycle, when rates hit 3.5% to 4.5% — levels that pushed monthly instalments to the edge of what many buyers could comfortably service, and effectively froze a significant portion of the market.

Here’s what that means in dollar terms.

Take a $2,000,000 condo, financed at 75% LTV over 25 years — a loan of $1,500,000. At today’s bank rate of approximately 1.7%, your monthly instalment works out to roughly $6,150. At the mid-2024 peak rate of 3.8%, that same loan cost approximately $7,750 a month. That’s a difference of $1,600 every month — $19,200 a year — or nearly $57,600 over a fixed 3-year tenure.

Let that number sit for a moment. The same property, the same purchase price, the same loan quantum — nearly half a million dollars difference in total cost, determined entirely by when you chose to borrow.

There’s a second implication that’s just as important, particularly for upgraders and investors stretching their budgets. Under MAS’s Total Debt Servicing Ratio rules, your maximum loan size is capped at 55% of your gross monthly income across all debt obligations.

Lower interest rates mean lower monthly interest expense, which means more room under that 55% ceiling. Buyers who were bumping up against their TDSR limits in 2023 may now qualify for significantly larger loans — without their income having changed at all.

If you were told two years ago that your budget couldn’t stretch to the property you wanted, it’s worth running the numbers again.

To be clear about the trade-offs: fixed-rate packages give you certainty for 2 to 3 years before you refinance, which is valuable if rates rise again. Floating SORA packages typically start lower but move with the market.

Neither is a set-and-forget arrangement — private property buyers should plan to refinance every 2 to 3 years to keep their rate competitive. That’s not a risk, it’s standard practice. And in the current environment, it’s a practice that rewards active borrowers.

What can be said with confidence is that today’s rates are historically favourable, and that buyers who lock in now have more certainty than those who wait for a further move that may or may not come.

Should you wait for private property prices to drop further?

Probably not. And the numbers make a compelling case for why.

The URA Price Index rose 0.9% in Q1 2026 — but as we covered, that headline masks a market where thousands of listings are sitting unsold and sellers are quietly negotiating.

The “crash” many buyers are waiting for isn’t coming in the way they imagine. What’s already here — motivated sellers, lengthening days on market, genuine negotiating room — is the correction. It’s just quieter than most people expected.

The opportunity cost of waiting is real and measurable.

If you’re currently renting a private unit at $4,000 a month while holding out for a further price decline, you’d need prices to fall by roughly $48,000 just to break even after a single year of waiting. On a $2,000,000 property, that’s a 2.4% decline — in a market where the price index is still technically rising.

Then factor in the rate risk. Fixed mortgage packages are sitting at 1.5% to 2.0% today. If macro conditions shift and rates climb back toward 3.5% — where they were just two years ago — the increase in monthly instalments on a $1,500,000 loan wipes out far more in savings than any modest price decline would have delivered. You’d have waited, paid rent, and still ended up paying significantly more over the life of your loan.

The supply window compounds this. The 58,000-unit pipeline giving buyers so much choice and negotiating leverage right now will be absorbed. Developers will sell through their inventory. Motivated resale sellers will eventually transact or delist. The market where you can walk away from a unit, find three comparable alternatives, and negotiate 3 to 5% below asking — that market has a shelf life.

That said, waiting is the right call if you’re not financially ready — if your downpayment isn’t in place, your TDSR headroom is tight, or a life event is coming that affects your housing needs. Those are real reasons to pause.

But if the only thing keeping you on the sidelines is “prices might fall a bit more” — the rent you’re paying, the rate environment you’re sitting out, and the negotiating leverage you’re not using are all working against you quietly, every single month.

Get your finances in order, get your In-Principle Approval done, and be ready to move when the right unit appears. In a market full of motivated sellers and genuine choice, preparation beats prediction every time.

So, should you buy private property in Singapore now?

Yes — and the window is more favourable than most buyers realise.

The pipeline is full, giving you genuine choice for the first time in years. The price index looks stable on the surface, but behind it sits a market of motivated sellers, stagnant listings, and real room to negotiate.

Financing costs are at levels that could save you hundreds of thousands of dollars compared to what buyers paid just two years ago. And the HDB upgrader pool — your competition for the same units — is entering the market with squeezed budgets and less urgency than before.

None of this is permanent. Supply gets absorbed. Rates move. Seller patience eventually runs out — in whichever direction the market tips. The conditions that make 2026 a buyer’s market are real, but they have a shelf life.

If buying a condo or a landed property has been on your mind, the question isn’t whether the market is perfect. It’s whether you’re ready to act while it’s working in your favour.

Talk to a Propseller agent today — get a free, no-obligation assessment of your budget, the right segments to target, and where the most motivated sellers are right now.